Transparency

The following report is produced in accordance with the Regulation of the Financial Supervisory Authority (FSA) no. 2/2016 on the implementation of corporate governance principles by entities authorized, regulated and supervised by the FSA, with the subsequent amendments and completions.

In light of the requirements of the regulations set out above, PAID S.A. publishes and periodically updates the information subject to disclosure requirements.

Download the document in PDF format.

A.Organizational structure

The management and administrative body of the company is carried out by: General Shareholders Assembly, Board of Directors/Management Board, Director-General and Deputy-Director General.

Shareholders:

The company's shareholders jointly own a number of 19,341,819 shares, with a nominal value of 4 Lei. Thus at present the share capital of PAID S.A. is at 77,367,276 lei value. The share capital of the company was increased during 2022, according to the Decision of the Extraordinary General Meeting (EGM) no. 2/27.06.2022, by increasing the nominal value from 1 Lei to 4 Lei for each share. Operation regarding the increase of the share capital was approved by the decision of the Financial Supervisory Authority no 1325/26.09.2022.

The appointed 5 members of the Management Board are:

Executive Management:

The management structure, in carrying out its own activity, benefits from the support of 8 advisory committees/boards: Risk Management Committee, Audit Committee, Claims Committee, Complaints & Dispute Analysis and Settlement Committee, Investment Committee, Reinsurance Committee, Business Continuity Committee (BCP) and Remuneration Committee. These committees operating on the basis of organizational and operational procedures hold regular board meetings throughout the year. These committees issue general recommendations on specific topics subject to decision-making and submit materials/reports to the Board of Directors regarding the subjects assigned to them by the latter.

At company level there are 8 Committees established: Risk Management Committee, Audit Committee, Claims Committee, Complaints & Dispute Analysis and Settlement Committee, Investment Committee, Reinsurance Committee, Business Continuity Committee (BCP) and Remuneration Committee.

The people holding key management positions are: Head of Risk Management Department, Compliance Officer, Head of Internal Audit Department and Chief Actuary - Head of Actuarial Department.

Organizational structure:

B.The main characteristics of the governance system

The governance system includes organisational structures designed to help achieve strategic objectives and activity of the company. PAID S.A is properly and efficiently organized, and all necessary operational controls and procedures are put in place.

PAID's governance system is based on an adequate and transparent distribution of responsibilities, which aims at an effective decision-making process, preventing conflicts of interest and ensuring efficient management of the company.

There are multiple systems in the company that have the role of ensuring corporate governance, such as:

A series of policies and procedures have been also adopted and implemented at the company level, including: policy to keep the business activities running smoothly, adequacy policy; remuneration policy; information security policy;

outsourcing policy; Solvency II policy; etc. These are subject to a regular review and approval process having regard to the nature, scale and complexity of the activities at both individual and corporate levels.

The Company's objectives regarding the corporate governance system are focused primarily on:

The organizational structure of the company and the Organizational and Operational Rules and Regulations demonstrate that the company has a structure appropriate to its nature, volume and complexity, and the principle of proportionality is respected. The ROF (Organizational and Operational Rules) also mentions the roles and responsibilities of the company's organizational structures.

There were no significant changes to the governance system during the reporting period.

Further details on the corporate governance framework are available in the Solvency and Financial Condition Report (SFCR) Chap. B.

C.Conclusions on the assessment of the financial position

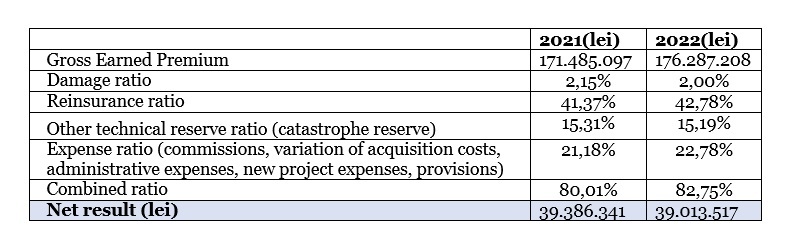

The key financial indicators of the company, according to the statutory accounting and financial reporting standards:

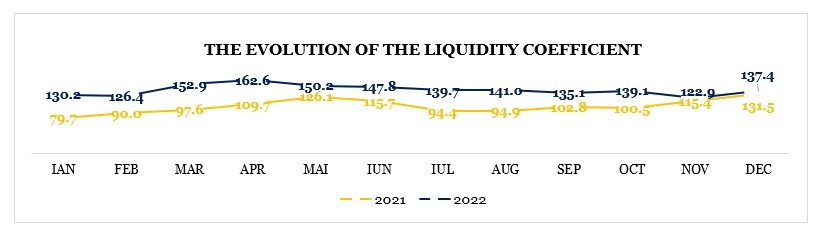

Evolution of the liquidity ratio, set out and calculated in accordance with FSA methodology:

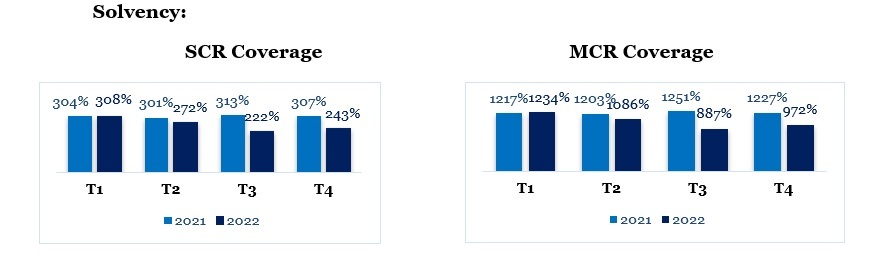

The main financial stability indicators of the company, in Solvency II reporting regime, calculated following the Standard Formula:

In 2022, the solvency ratio followed a downward trend determined by both the increase of SRC as a result of increase in own funds and by reducing own funds accruing from own resources as a result of the fall in market value of treasury bonds, generated by the unfavourable developments of the interest rate.

To cover catastrophe risk, PAID S.A. as of 31.12.2022 had a reinsurance program of a 1 billion EURO capacity for earthquake, flood and landslide risks, its own retention being limited to 11 million EURO for earthquake risk and 9 million EURO for landslides and floods risk. The reinsurance program is supported by a panel of 48 reinsurers, and approximately 50% of the capacity comes from reinsurers with “AA” ratings granted by S&P or AM Best.

D.Main characteristics of the formal framework for the implementation of financial reporting principles and practices

PAID S.A. draws up statutory financial statements in accordance with the Financial Supervisory Authority Rule no. 41/2015 for the approval of the Accounting Regulations on the annual individual and consolidated financial statements of entities carrying out insurance and/or reinsurance activities.

The annual financial statements are audited by an independent auditor. The financial statement package for the fiscal year of 2022 was audited by Mazars România SRL.

In accordance with the provisions of ASF Rule No. 19 / 30.10.2015, the company, starting with 2015, establishes and publishes annual financial statements for information purposes in applying international financial reporting standards (IFRS).

Solvency II Reporting (SII)

In accordance with the financial reporting requirements under Law No. 237/2015 relating to the authorisation and supervision of insurance and reinsurance activities and under Regulation No. 21/2016 on reports concerning insurance and/or reinsurance activities, with subsequent amendments and additions, PAID S.A. draws up and reports:

In addition, in accordance with the provisions of Solvency II, the Delegated Regulation and Internal Policies, PAID S.A. draws up each year, or whenever significant changes occur in its risk profile or risk appetite, a prospective own-risk and solvency assessment report conducted at group level (the ORSA report).

At PAID S.A. level a „Reporting Policy” has been developed and applied, which aims to ensure in due course the achievement and transmission of all mandatory reports, as well as that the information provided is correct and complete.

The Audit Committee is the forum that delivers opinion on statuary and that of Solvency II reports, prior to these being submitted to the Management Board and/or General Assembly for approval, as appropriate.

E.Main characteristics of the risk management system

The Risk Management System at Company level is carried out through the planning,

coordinating and controlling of the Risk Management activities. Within this

framework, specific strategies are established, policies and procedures are developed

for the timely identification, assessment, monitoring, management / reduction and

reporting of risks, with the aim of optimizing these and creating a “risk-aware”

organization culture.

Through the risk management system the objective is to ensure the achievement of the company's objectives regarding: strengthening Solvency II;

The specific risk management strategy is an integral part of the company’s general strategy, having as main fundamental objectives: meeting SCR and MCR capital requirements and ensuring increased solvency ratio, achieving an optimum reinsurance programme and effective profitability- and capitalization-oriented management, with the unitary purpose of maintaining PAID S.A.’s financial stability.

PAID S.A. establishes an annual risk plan in which objectives and measures are presented for each and every significant risk, submitted for debate and approval of the Management Board/Board of Directors.

The PAID risk strategy is based on the following main principles:

With regard to development and performance trends, the Company has established the main objectives for 2023-2027, related to the 4 pillars of development, according to the Business Plan:

1. Governance: ensuring an operational framework fully consistent with legal requirements and the risk profile of the company;

2. Financial sustainability: reflected by the company's solvency level and the appropriate size of the structure and level of reinsurance protection;

3. Operational sustainability: reflected in the ability to cope at any time with a number of operations much higher than the usual average in the event of major events or in case of increasing portfolio;

4. Development: increase of the penetration rate and by default of the portfolio.

The activity of PAID S.A. is analysed in terms of exposure to the following risks:Underwriting Risk, Liquidity Risk, Credit Risk, Market Risk, Operational Risk, Reputation Risk and Strategic Risk. Risks are treated both on an individual and aggregated level. PAID S.A. calculates the capital requirement using the Standard Formula. The results obtained provide an overview of how risks are divided into various risk categories and determine capital and solvency requirements in accordance with Solvency II.

Based on the financial results of recent years, PAID is in the process of accumulating own funds and optimizing the capital requirement to ensure a more comfortable solvency ratio.

Risk analyses are drawn up at company level in accordance with the specifications of risk policies and procedures.

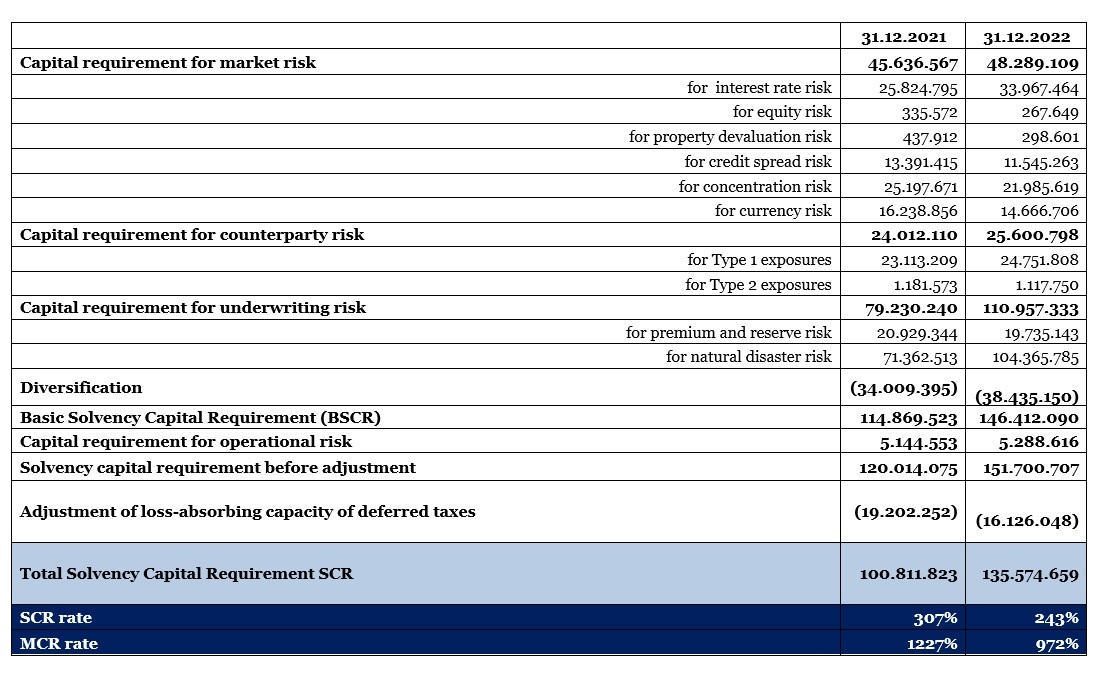

The quantitative assessment of the Solvency Capital Requirement is:

More details on the risk management system are presented in the Solvency and Financial Condition Report (SFCR) Chapter B (subchapter B.3) and Chapter C .

F.Conclusions of the assessment of the efficiency of the risk management system

Pregătiți să reconstruim împreună

RO

RO HU

HU